There has been a precipitous decline of betting on the Totalisator which gives cause for concern for the horseracing industry. In the 1990’s, the tote accounted for 66% of ALL betting in South Africa.

Robin Bruss writes that today it accounts for 0,3% of ALL betting in South Africa.

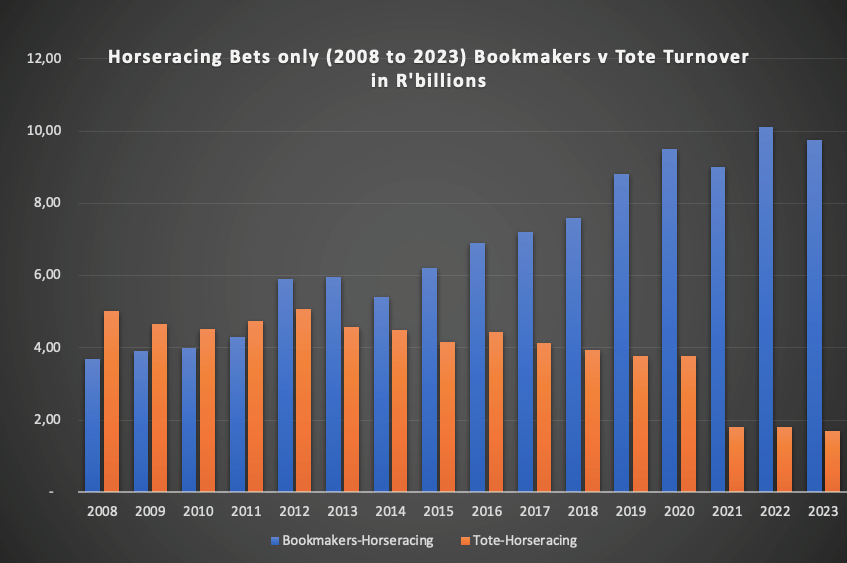

More importantly, in terms of betting on horseracing only, in 2023 the betting market share of the Tote was 17,4% (at R1,7 billion) compared to the Bookmakers 82,6% (at R9,75 billion). This is the reverse of what used to be.

I can’t say that this essay is a complete authoritative study. The subject is much bigger than one article and has multiple facets. I hope that some of the facts that I am able to show, and some of the observations I have made will resonate, and stimulate further discussion and thinking as we eke our way forward to a better model of racing’s future.

Here goes:

The Tote was the dominant form of betting in South Africa until 2012, when bookmaker’s bets on horse racing surpassed it for the first time at around the R4,5 billion mark. Since then, bookmaker’s bets on horseracing have more than doubled. The Tote by contrast has more than halved.

The Concern For Racing

Those of us in racing are concerned, because traditionally for more than a hundred years, the Tote has been the provider of the income stream on which horseracing was regulated, organized and operated, and its prize money paid.

In short, it is the Tote on which we have traditionally relied to keep racing stabilised. It is the Tote’s contribution to prize money which largely informed the yearling and racehorse market, which thereby enable the employment of staff on breeding farms; its contribution to purses stimulate all the employment of participants in the Sport, the staffing of operations of the turf clubs.

There was a time when the tote fully funded the regulatory authorities, plus the lion’s share of the training of jockeys and work riders, and funded its own betting operations.

Without the tote income, the costs of running racing and paying purses has to be found from other sources, and so it has come to be in recent years – with the lion’s share currently coming from the pockets of philanthropists, and bookmaking ventures.

Consider that the Tote has significantly large deductions from the Pool. In most countries where Totes operates, Win and Place pools have between 14% and 16% deducted before declaration of the dividend. In two horse bets such as the Exacta or Dupla, it’s around 25%, and in the big exotic pools like the Pick 6 and Jackpot, it’s between 25% and 30%.

It was able to do this because of one word: LIQUIDITY.

Pools were so much bigger than what Bookmakers could hold, and liquidity was so much deeper that even after the fat deductions, the dividends to punters could be traditionally larger.

This was especially true in the case of the exotics such as the Pick Six and the Jackpot, which at times in days gone by, had payouts that looked more like a lottery windfall.

The Tote was meant to have the tools to compete but, as we have seen, it has been on a downward spiral for the last 28 years.

So what changed ?

Understanding the Regulatory Framework

In the period from 1948 to 1998, the Tote maintained its advantage by betting licensing being controlled by the Jockey Clubs and Bookmakers had to apply to the Head Executive of the Jockey Club (now the NHA) for a licence.

If memory serves me correctly, the order was maintained at around 60 bookmakers’ licences country wide.

All of that changed with the New South Africa in which the Wiehann Commission (1993) recommended a new dispensation for widespread gambling which would include Casinos, slot machines, Bingo and a National Lottery, competing with horseracing.

One of the inducements in setting up the public company Phumelela, was to provide racing with a modern way of competing with other forms of gambling.

The tote was allowed reductions in taxes to try and make it more competitive, and the first Sports betting licence was issued to the Tote for the set up of Soccer Pools.

The National Gambling Board was set up for the regulatory and licensing of all gambling which was then outsourced to each Provincial Gambling Board.

Although there is supposed to be a national policy framework, what happens in practice is that each Provincial Gambling Board issues licenses for its province, they determine tax rates for their province, they collect betting taxes at various differing rates depending on what they deem suitable for their province.

Today there are some 380 bookmaker’s licences and around 600 bookmaking outlets countrywide.

Distortions in the Provinces

The differing rates and allowances have led to distortions.

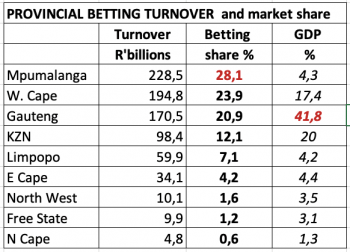

For example, Mpumalanga has a 4,3% share of the national economy, but it leads the whole country by betting in 2023 with a 28% share of all gambling. They report turnover of R229 billion, despite being only the 5th richest province of all nine provinces.

By comparison, the richest province, Gauteng, accounts for 41% of the national GDP, but only 20% share of all gambling with an aggregate turnover of R170 billion.

KZN is the second richest province with 20% of the national GDP, but ranks only 4th in betting with just 12% of all gambling.

For little Mpumalanga, who have a population (2022 census) of 4,9% of South Africa, and a GDP of 4,3%, how is it possible for them to have 28% share of the National Gambling market, but for them providing such an advantageous regulatory framework for big gambling operators, that they are sucking away betting from other provinces far richer than them?

The matter of different regulations and licencing in each Province is a fascinating study in itself. We will save the subject for another day. Suffice to say that, although the Constitution of South Africa demands a harmonization of the law, the fact is that Provinces have a widespread autonomy and different dispensations abound

The effect of this, when you start to analyse what it may mean in practical terms for horseracing, is that you discover two things:

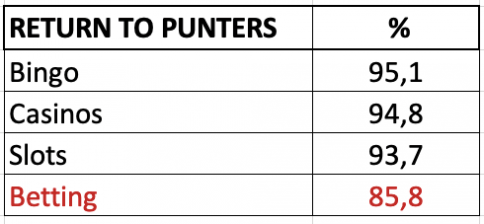

- The Return to Punter in horseracing bets on a national level, especially on the tote, is a big disadvantage.

2. That according to the 2022/23 National Gambling Board statistics, the total taxes paid by Bookmakers AND the Tote on HORSERACING betting was EIGHT TIMES the rate paid by SPORTS betting.

The regulatory and tax anomalies for horseracing require introspection and revision, both provincially and nationally.

The National Gambling Amendment Bill

In 2006, the Department of Trade & Industry commenced a review in order to update and harmonise gambling legislation.

This led to a National Gambling Review Commission (NGRC) under the chairmanship of Ms Joan Fubbs, with presentations given in parliament by various stakeholders, including the writer, who presented an industry outlook on behalf of the NHA.

The distortions in taxation rates was referred to, but Minister of DTI, Rob Davies, issued a press release in 2013 to state that Government was aware, but required the horseracing industry to deal with transformation first.

The NGRC released a report which contained various recommendations on a national framework on all gambling policy.

This led to a White Paper in 2015 calling for public comment on provisions of the new National Gambling Amendment Bill, followed by the final draft coming to Parliament in 2018 and again in 2021 and being returned both times as inadequate and incomplete.

The new draft has yet to be issued – the gambling landscape is changing so rapidly with new bet types and digital expansion, that the Act has yet to keep up.

It is therefore possible for racing to review its own position and make representations for further amendments.

The Tote as a System of Betting

THE TOTE is a glorious system of betting in countries when it is protected from competition by legislation.

They include most notably, JAPAN, HONG KONG, FRANCE and USA. They fill four of the five top countries ranked by prize money paid.

In many countries where the Tote must compete with bookmaking, the tote has a greater struggle. The obvious reasons are that bookmakers have the advantage of offering credit, they are permitted a wider variety of bets, can offer discounts or stretched prices, and many other inducements, with known outcomes.

The tote is heavily negatively influenced by a single large bet if the liquidity of pools is low, and that weak state of liquidity is becoming more prevalent in South Africa as turnovers slide downhill.

One way of overcoming this was to create a National Tote (SAFTOTE) in which all betting on the tote countrywide is mixed into a single comingled pool.

A second way was to mix that co-mingled pool with the international totes to which South Africa is beaming its product.

Although Phumelela was the pioneer in taking South African racing to 40 other countries, its effect on local totes appeared negligible. Its global dissemination was through an offshore vehicle, Phumelela-Gold, owned at the time with Gold Circle and in partnership with British Racing (GBI) and Australia’s Tabcorp.

Its revenue was reflected in Phumelela’s Annual Financial Statements as ‘Intellectual Property Fees’, effectively the recording of media rights.

Hong Kong Jockey Club’s World Pool is a global initiative in which the host country several times a year beams its racing into the global broadcast and on which Totes around the world co-mingle their tote pools with the host country receiving a large commission. It is extremely profitable for the host country.

For example, the British Tote reported in 2023 that because of the World Pool, the British Tote’s turnover in 2022 grew by 44% to a figure of £521 million turnover.

South Africa’s signal festival events such as the July, the Met, the Summer Cup and Champions Day are all part of the World Pools now.

Liquidity remains an issue for the Tote in South Africa and is one of the factors causing its slide.

Other Factors affecting the Performance of the Tote

I’m going to express some personal observations, not reliant on full quantitative facts and analysis, but a current estimate of some things that might have altered the balance against the Tote:

1. Lack of focus and reduction in the number of tote outlets.

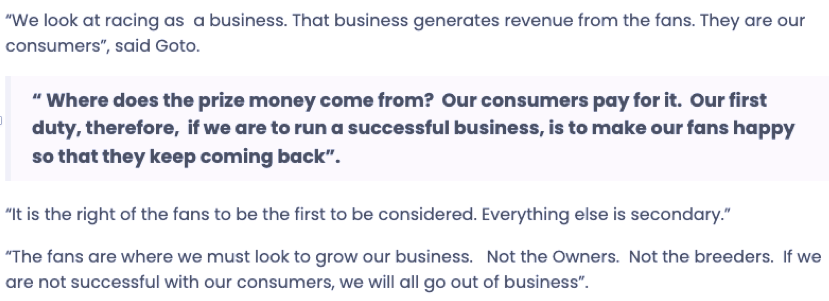

2. Lack of media dissemination and appropriate information to the rank and file of punters, who lost faith in the product of horse racing.

Punters are not kept informed to the same standards of operators like the HKJC and the JRA, which make it a hallmark to put the punters first.

The words of the Japan Racing Association Chairman Masayuki Goto at the Asian Racing Conference in South Africa 1995 remain pertinent:

3. Failure to be the leader in the astounding rise of online betting on smart phones. Bookmaker and Casino platforms are far more advanced.

4. The tote’s branding is weak, with mixed messages – the branding is for TAB, which means what – ‘Tote Agency Board’, or sometimes advertised as ‘Take a Bet’. In Durban it’s called TABGold, but the tote in all the provinces is referred to as SAFTOTE. We talk about having a Tote bet, but the online betting platforms say TAB.

Bookmakers offer fixed odds, but they also offer Tote bets in a system called the Open Bet, which invariably, except for some egalitarian bookmakers, don’t put the bet into the pool, but will pay you out the same dividend as the declared tote (err.. TAB) dividend, unless it’s a big exotic dividend – which they don’t because they have limits on what they will pay.

5. I’m a racing man but even I get confused where to study the form between the NHA’s pdf results posted to a site no one looks at; TABGold used to publish results pages, now you have to look at a site called Gallop.

I don’t know where 4Racing publishes results, I use independent group Formgrids.org, others use Racebook.co.za; the local newspapers don’t publish results, other than numbers of the horses with payouts but no names of the horses and definitely not the connections names, not even jockey or trainer.

6. Trying to watch the races is also not easy. 4Racing and Gold Circle have different channels, not all races are even on DSTV. By year end, 4Racing will only have Gauteng and East Cape racing on their DSTV channel, because, as I understand it, the contract with Cape Racing and KZN expires.

Getting to live stream is good but challenging, as the channels require gateway password access, and if it’s a hassle for me, it can’t be easy for the masses.

To me there is no doubt that the MARKETING of the tote, and even of horseracing is a MISH MASH, capable of confusing even the ardent fans.

In this regard, I am not surprised at the decline of the Tote.

Given the media coverage of the major bookmakers, their sponsorships, their customer related marketing, it’s clear that they create loyal fans, and so they now control 82% of the horseracing betting market.

A new look at a racing media division is advised, not only to promote the horse and protect the tradition and history of the Sport, but also to align it to betting.

In this respect, organisations such as the Racing Association and the Thoroughbred Breeders Association ought to put on their agenda ways in which to preserve and protect the ETHOS of the Sport.

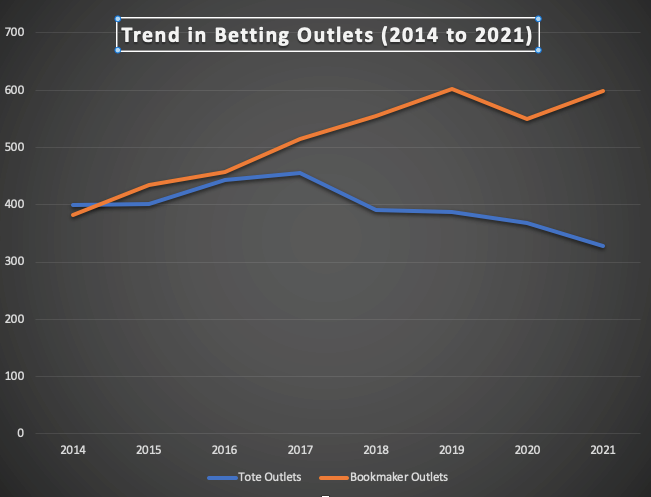

Reduction in Tote Outlets

Over the 10 years period to 2021, there has been a steady decline in the number of Tote outlets, whilst bookmakers have almost doubled their reach. Whilst significant, bricks and mortar outlets as platforms have been dwarfed by the explosion of mobile betting.

Source: National Gambling Board 2023, but figures for 2022 and 2023 not available.

Global Digital Insights noted that in 1998, mobile phone penetration was 9 million phones of about 18% of the population of South Africa.

In 2022, it is over 100 million or 176% of the population. Of these 80 million are Smart Phones, capable of data platforms on which betting is possible.

The Open Bet occurs when the Bookmakers lays the equivalent to a tote bet but holds the bet himself rather than submitting it into the tote pool. He promises to pay the same dividend as the Tote and risks that if the punter wins, he loses and must pay the equivalent dividend as declared by the tote.

Effectively the Open Bet deprives the pool of the turnover it would receive and similarly it avoids the takeout ordinarily used to fund the operator, pay the prize money and provide for government taxes.

If the punter loses, the bookmaker scoops his whole bet as there was no requirement to pay it into a pool.

Let’s take a look at the open bet:

The Open Bet

The open bet has been in play since it was approved by an Ordinance in 1961.

Various highly speculative estimates have been given as to the level at which the Open Best takes revenue away from the Tote. I have yet to see or been able to find any published quantification.

The principle of the Open Bet was examined and its impact discussed in both the High Court and in the Appellate Division when Phumelela sued three bookmakers in an attempt to overturn the current law allowing the open bet in a bid to protect the Tote.

The case is known as Phumelela v Grundligh, Schuler and Turfsport cc (2005).

Phumelela charged that Bookmakers were licensed to offer Fixed Odds which are clearly defined as having an agreement of the winnings in advance of the race.

By offering equivalent payouts for Tote Bets, for which the dividend could only be declared after the race was run, they charged that the bookmakers had contravened the definitions of the National Gambling Act 1995.

The High Court agreed, the Appellate division did not and overturned the High Court judgement.

The three judges of the Appellate division found that that the definition of Fixed Odds also included the notion of a bet struck on the basis of the horse’s Starting Price, for which the winnings could not be known in advance but only after the race.

In considering the function of the Open bet, they deemed its principle of paying a dividend after the race when in became calculated to be a similar or the same as the starting price payment and they overruled the High Court judgement.

Interestingly, the Appellate division also had to decide if such a practice was unfair and unlawful in order to consider if the law should be amended. Just because something may be unfair, it does not necessarily mean it is unlawful.

In determining the difference, the defining point lies in the public interest.

Judge Comrie described the perceived unfairness thus –

“Reduced to these essentials the parasitic nature of the appellant’s exotic bets is in my view, plainly evident. There is no fear that the parasite will kill the host, but competing on these uneven terms, there can be little doubt that in accordance with the laws of nature and business, the parasite will likely harm the host, as parasites usually do. I consider that right thinking members of the community should and would condemn it without much ado.”

“All that can be offered in defence of the practice is that it has been legislatively sanctioned for many years (1957, 1961, 1978 2004) (even though) such bets remain essentially parasitical. In my view they reap an unrighteous competitive harvest, they are legally unfair.”

However, Judges Farlam and Conradie did not agree with Comrie. Whilst they understood it may not be particularly fair, they determined that it was not ‘unlawful because of the history’.

The law permitting it had been in place in Natal since 1957, permitting bookmakers to offer “bets at Tote odds”. This stance was repeated in the National Horse Racing and Betting Ordinance 24 of 1978.

The replacement legislation, the National Gambling Act 4 of 1995 did not prohibit the Open Bet, but then the Gauteng Gambling Act 1998 did, excluding bookmakers from ‘offering a tote bet of any kind’.

However, this was then reversed in the National Gambling Act 2004 which specifically permits an Open Bet.

Given introspection and examination and confirmation many times by legislative bodies means it is a long standing law, and if the public interest was so assaulted in the past 50 years, why had only one objection come to the court in this long period?

After the Appeal Board’s decision in 2005, the discussion came up at the 2012 NGRC hearings on gambling policy in parliament. Apart from noting that horseracing was entitled to some form of payment by bookmakers for use of their IP in betting, no recommendation was made to amend the Open Bet and it did not appear in the White Paper 2015.

What effect would a change to Open Bet have for the Tote?

Currently the big bookmaking chains are supporting horse racing to the hilt despite the fact that racing accounts for altogether R9,7 billion out of Bookmakers total turnover of R427 bn turnover. That is 2.2% of their business. How much of that total might constitute the Open Bet?

At the moment, the figures are highly speculative: we don’t know. If there is evidence in someone’s possession, let’s hear it.

The Operators and Bookmaking chains might find it useful to seek clarity and decide if there is merit to re-visit and if so, who would support the amendment to the Bill and to consider what the Tote or the Sport of Racing might have to gain by it.

Alternatively, it might even be a lesser sum than the big bookmaking companies are already giving to racing, and if that is the case, it will be dead before it can begin.

Where to From Here for the Tote?

It’s going to be interesting to ask both Cape Racing’s Greg Bortz and 4Racing’s Chairman Charles Savage and CEO Fundi Sithebe to provide their views on the way forward with the Tote, as they seem to have polar opposite views on the matter.

Cape Racing eschews the Tote in its current form as being capable of turnaround and enhancing the sport of horseracing as it used to do.

They have hitched their future to a ‘partnership’ with South Africa’s biggest bookmaking chain, Hollywoodbets, and they have some well stated innovative plans – and there are others in the wings which use the principle of a Tote license but create a different operational pathway.

4Racing eschewed the bookmaker’s licenses in its purchase of Phumelela’s assets and the tote, but not the bookmaking operations they held in Betting World and Supabets. Whether 4Racing can turn the tote around, or has alternative plans, deserves a different article.

What is true, is that creativity and entrepreneurial capability abounds, especially given the vastness of the new technologies which already have commanded the incredible rise of betting with a 10 000% growth path.

How to tap into it is the new frontier and to boldly go where no man has gone before (to borrow a phrase from Star Trek!) provides both hope and excitement.

By the way – have you read part 1 of this series? Click here.

Before closing, one more point regarding the structure of racing and sport:

Alternative Funding of Other Major Sports

Most Sports are organized differently to horseracing’s reliance on gambling.

Soccer, Rugby, Cricket, Tennis, Basketball, Golf, Motor racing and major league sports all depend largely on media rights (television and internet) because they command a massive viewership, and the bigger the drawcard of public viewership, the greater the fee that sports commands.

Multichoice announced a broadcast rights deal with the Premier Soccer League to pay more than R1 billion p.a. for television and internet rights. The Rugby Championship (South Africa, New Zealand, Australia and Argentina) is worth several hundred million dollars p.a. American Football commands $10 billion p.a!

No such luck for racing here, whose income has traditionally been from gambling, and is obliged to pay its own way to be on television.

The challenge is for racing to be so popular that broadcast channels will pay for the right to broadcast. Or for Sports to find a way to earn revenue from the massive gambling which we see taking place on it.

The changing landscape already sees a blurring of the lines.

The Jockey Club in UK established an alternative model. It’s as a non-profit body by Royal Charter and all of its profits flow back into horseracing.

It owns 14 racecourses and no betting outlets.

The racecourse and the festival meeting they operate include some of the most iconic in the history of horseracing such as Epsom Derby and Oaks; Aintree’s Grand National; Royal Ascot, and Newmarket’s Classic races.

The Jockey Club’s sale of media rights for these events runs to more than £200 million (R4,6 billion) p.a. which is more than double the £99 million contributed by the Horseracing Levy Betting Board in 2023, from bookmaker betting.

Media rights are based on popularity, and its popular appeal to the public that drives every sport whether its income is betting based or media based.

Perhaps one of the keys is the simplest as Japan has proclaimed. Use the best of media and latest technological systems to create a customer-centric operation. Make it personal and let them identify with the stars of the sport, reach them with interactive systems as we see similarly in F1 motor racing and other sports, use AI to tailor make and personalize the approach. Find new revenue drivers.

We are already living beyond Huxley’s proverbial Brave New World in technological advances. We can, and must, step forward and these articles will continue the series to look at what we have and where we can go.

Ed – Author Robin Bruss is away overseas for a few weeks. We look forward to part 3 of this series on his return.